WE HAVE MOVED TO OUR NEW OFFICE LOCATION AT 215 - 1540 CORNWALL RD, OAKVILLE

How Investment Income Is Taxed Inside Your Corporation - And Why It Matters

FINANCIAL PLANNINGTAX PLANNINGWEALTH MANAGEMENTCORPORATE TAX PLANNING

Matthew Watt

2/1/20264 min read

If you're a business owner with retained earnings or investments sitting inside your corporation, you may already know that pulling that money out comes with a significant tax bill. Many owners choose to leave funds inside the corporation and let them grow — but here's what's often overlooked: how those funds are invested makes an enormous difference to your after-tax outcome.

Let's break down how corporate investment income is taxed in Canada, and what you can do to keep more of your money working for you.

The First Thing to Know: Corporate Investment Income Is Taxed Hard

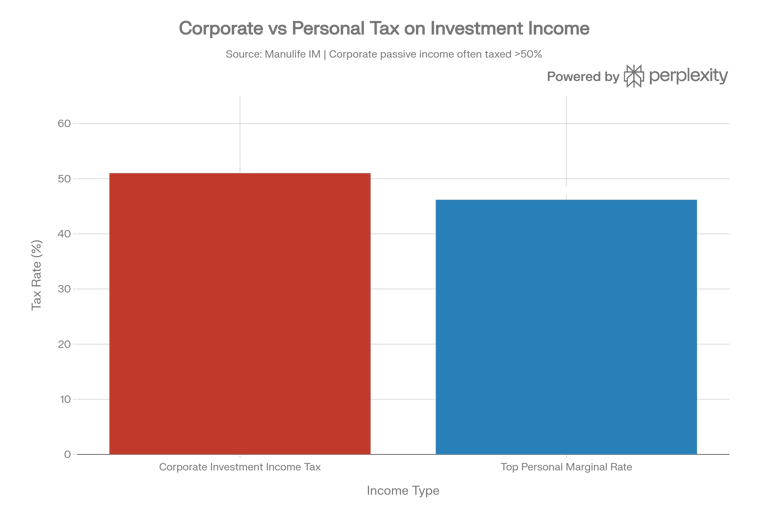

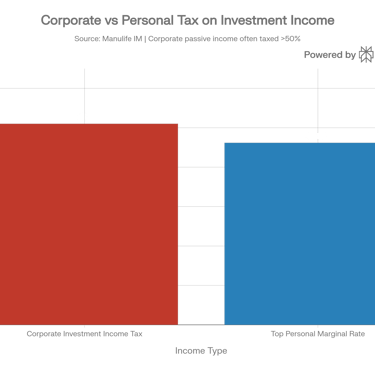

Unlike active business income, which benefits from graduated rates and the small business deduction, investment income earned inside a Canadian-controlled private corporation (CCPC) is taxed as passive income at a flat rate — and that rate often exceeds 50%, depending on the province .

To put that in perspective: the top personal marginal tax rate in Ontario is approximately 46.16%, while corporate passive income can be taxed at 51% or higher. That means your corporation is not a shelter for investment income — it's a high-tax environment if you're not investing strategically.

Not All Investment Income Is Created Equal

Here's where smart planning makes a real difference. There are three main types of investment income inside a corporation, and each is taxed differently:

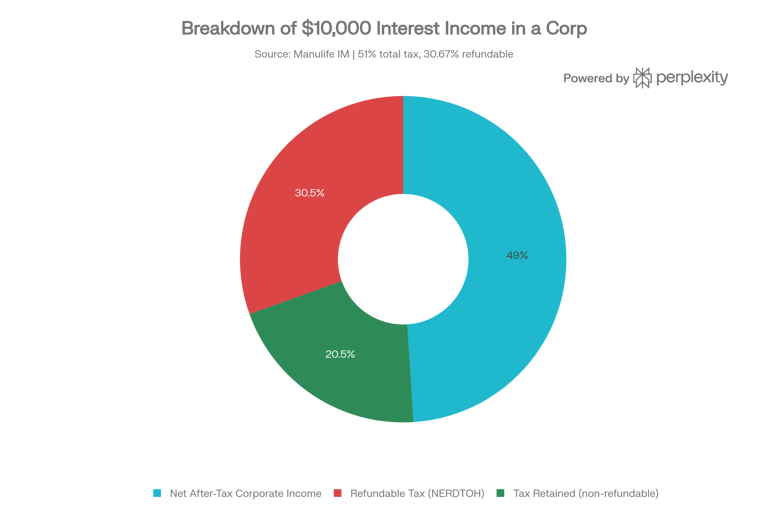

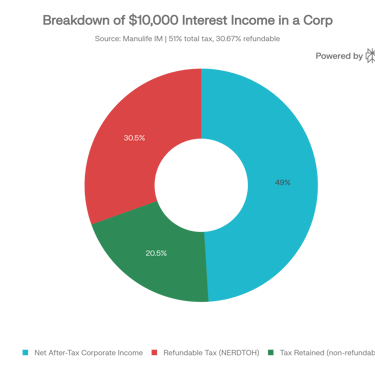

1. Interest Income & Foreign Income

This is the least tax-efficient category. Interest from GICs, bonds, or savings accounts — as well as foreign dividends — is fully included in taxable income and taxed at the full passive income rate (up to 51%) . A portion (30.67%) is refundable and tracked in the Non-Eligible Refundable Dividend Tax on Hand (NERDTOH) account, meaning it can come back to the corporation when taxable dividends are paid to shareholders.

2. Capital Gains

Capital gains are much more tax-efficient. Only half of a capital gain is taxable, meaning a $10,000 capital gain only generates $5,000 in taxable income . The non-taxable half gets added to the Capital Dividend Account (CDA) — a powerful tool that allows shareholders to receive those funds completely tax-free as a capital dividend.

3. Canadian Eligible Dividends

Dividends received from other taxable Canadian corporations are subject to a 38.33% refundable tax, all of which is tracked in the Eligible Refundable Dividend Tax on Hand (ERDTOH) account . This tax is refunded when the corporation pays eligible dividends to shareholders.

The RDTOH Mechanism — Getting Tax Back

The refundable tax system is designed to prevent corporations from gaining a permanent tax advantage over individuals investing directly. Here's how it works:

When your corporation pays a taxable dividend to you as the shareholder, it receives a refund of $1 for every $2.61 of dividends paid, up to the balance in the applicable RDTOH account . That refunded tax then flows out to you, the shareholder, where it's included in your personal income and subject to the dividend gross-up and dividend tax credit system.

The key takeaway: the refundable portion isn't "lost" — but it only comes back when dividends are paid, meaning the timing and type of income matters.

The Capital Dividend Account: A Tax-Free Exit Strategy

The Capital Dividend Account (CDA) is one of the most underutilized tools in corporate tax planning. It's a notional (tracking) account that accumulates the non-taxable half of all capital gains your corporation realizes . The corporation can then elect to pay out a capital dividend up to that CDA balance — and the shareholder receives it completely tax-free.

Pro Tip: If your corporation has a CDA balance, consider paying it out promptly. If left untouched, 50% of any future capital losses will reduce the CDA — eroding your future tax-free dividend room .

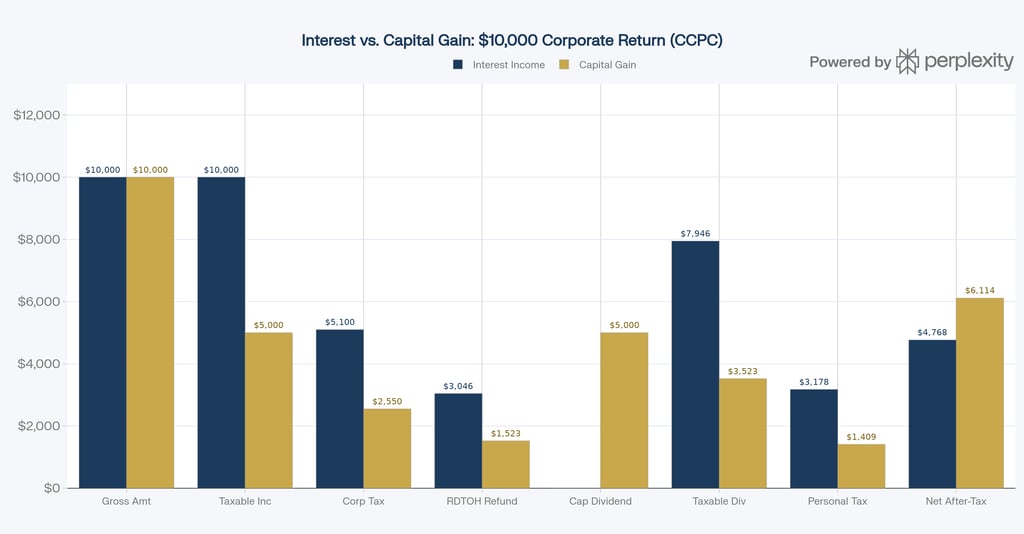

Dollars and Sense: Interest vs. Capital Gains Side by Side

Let's look at a practical example using a $10,000 investment return inside a corporation at a 51% corporate tax rate, with a 40% personal dividend tax rate on the shareholder side:

The difference is striking. By earning capital gains instead of interest income, a shareholder could receive nearly 28% more after-tax income on the same $10,000 — simply through tax-efficient investing .

What This Means for Your Investment Strategy

If your corporation holds cash or investments, every dollar should be working as tax-efficiently as possible. Practically speaking, this means:

Prioritize investments that generate capital gains (e.g., equity portfolios, growth-oriented ETFs) over those that generate interest income (e.g., GICs, bonds, savings accounts)

Monitor your CDA balance and work with your advisor to pay capital dividends promptly before potential capital losses erode the account

Understand your RDTOH balances (both NERDTOH and ERDTOH) and coordinate dividend payments to maximize tax refunds to the corporation

Work with a financial advisor and tax professional together — the interplay between corporate and personal tax is complex and highly individual

The Bottom Line

Leaving money inside your corporation isn't just about deferral — it's about strategy. The type of investment income your corporation earns, and when and how it's distributed to you as a shareholder, can mean tens of thousands of dollars in tax savings over time.

At RBIA, we help business owners and professionals navigate these complexities as part of a comprehensive retirement and financial planning strategy. If you're unsure whether your corporate investments are structured as efficiently as possible, it's time to have that conversation.

Get in touch

Address

Retirement Benefits Insurance Agency Ltd.

1540 Cornwall Rd - Suite 215

Oakville, Ontario, L6J 7W5

Contacts

905-847-7474 - Phone

905-847-9791 - Fax